Friday, December 12, 2014

Norges Bank Not Worried About Rising Home Prices

I actually think Norges Bank is factoring in a very high probability for a recession in 2015 (Olsen basically said it out loud, "severe downturn"), so I don't understand the current fuzz about higher home prices and Norges Bank having abandoned their push for lower household credit growth. They must think that they will get lower credit growth anyway, and the rate cut is actually aimed at softening the expected fall in lending to businesses and households.

The Norwegian Krone has already fallen so much, so fast, that I don't see this 0.25 per cent cut had that much to do with lowering the exchange rate. From any non-short-term exchange rate point-of-view, it didn't really matter if they cut now or in March 2015. Had they not cut now, it would have been more likely that they cut 0.5 per cent in March. That would have been, at least partly, reflected in market expectations.

The timing of the rate cut matters much more for private sector credit growth, and this cut is about conveying a message of looser monetary policy to that sector, to keep the credit growth from following the outside temperature too closely now that winter is coming (it's +1 degrees in Oslo today...).

It's time to wake up to reality: Norges Bank is not anymore worried about rising home prices. If anything, they are worried about falling lending -- both demand and supply-driven-- to businesses and households, and eventually falling home prices.

As Keynes knew, "animal spirits" play a much bigger role in business investment decisions than any interest rate changes Norges Bank is able to create from an already low level. So we can expect that household lending is the area that is affected the most by this rate cut. But really, do they believe such a small cut would offset the effect of negative psychology, witnessed in steeply falling consumer expectations (in Norwegian, but see graph)? I think we are seeing here again the mental model many Norwegian economists have managed to build in their heads: Home prices just can't fall.

Thursday, December 11, 2014

Norges Bank Trying To Stay Ahead Of The Curve

Norges Bank unexpectedly cut its "steering rate" today from 1,50 % to 1,25 %. It stated the following as a justification for its decision which somewhat surprised the markets (via Richard Milne -- @rmilneNordic -- at FT.com):

Some economists and other pundits, Øystein Dørum of DNB Markets and Atle Willems of EcPoFi among them, have argued that this is "wrong kind of medicine", as they expect that it might lead to increased lending to households, and higher home prices. Of all the people, I should find myself in agreement with them. And I can't say that I strongly disagree. I just don't think it's as simple as that.

I believe there's a good chance that Norges Bank is much more worried about the economy than most of us realize. One sign of this is how they today expressed their concern for the world economy:

As of late, one of the main arguments for an expected soft landing in Norway has been the strength of world economy, a factor which, combined with a weaker Krone, is expected to help Norwegian non-oil exporters. The oil price fall has been widely interpreted as being supply-related, which would mean it would stimulate oil-importing economies. That is a dangerous over-simplification. You can never forget the demand side, and there it is expectations that matter. China, one of the main locomotives of world economy since 2008, has been slowing down for a while and this trend is expected to continue in 2015. Europe is another headache that won't go away, and it's the destination for around 80 % of Norwegian exports.

It has been suggested that today's rate cut is a sign of strong pessimism on the part of Norges Bank, and I can't but agree. To be fair, Dørum of DNB says that if credit growth would slow down substantially, then a rate cut could be the right choice. Whereas he would like to see more evidence before the cut, Norges Bank has decided to act already on the expectation of much slower credit growth. In other words, it's trying to do "whatever it takes" (please, Mr. Olsen, don't ever use those words...) to stay ahead of the curve.

I see also a human factor behind this decision. This might come as a revelation for some of the readers, but central bankers are human beings like the rest of us. To better understand what they might be thinking at Norges Bank, I suggest you read this article from the Financial Times: "Central banks: Stockholm syndrome". It shows how Sweden's Riksbank, and especially its head Stefan Ingves, has been crucified -- by Paul Krugman and the likes -- for too tight monetary policy, the aim of which was to fight credit growth and higher home prices. I do recognize that the inflation and unemployment situation is different in Norway at the moment. But so is it with GDP growth (6,6 per cent in Sweden back in 2010!) and the expectations thereof. My point is a broader one: In the current environment, the prevailing (academic) opinion -- which I disagree with -- makes it very likely that central bankers will get punished for anything that in retrospect turns out to be too tight monetary policy. This has happened to Riksbank under Ingves in 2010 and the ECB under Trichet in 2011.

Whether we like it or not, the "easing bias", much critized by the Bank for International Settlements, is still there. But I can live with a 0,25 point cut, which I don't expect to be enough to keep the credit flowing freely to households now that the severity of the economic situation is finally dawning on the public. Should I find myself mistaken on this one later, I promise to curse today's rate cut!

UPDATE: Olsen puts it like this at Bloomberg:

“Growth prospects for the Norwegian economy have weakened. Activity in the petroleum industry is softening and the sharp fall in oil prices is likely to amplify this tendency. This will have spillover effects on the wider economy and unemployment may edge up ahead. At the same time, the krone has depreciated markedly, which is helping to dampen the effects on the Norwegian economy and underpin inflation.”

Some economists and other pundits, Øystein Dørum of DNB Markets and Atle Willems of EcPoFi among them, have argued that this is "wrong kind of medicine", as they expect that it might lead to increased lending to households, and higher home prices. Of all the people, I should find myself in agreement with them. And I can't say that I strongly disagree. I just don't think it's as simple as that.

I believe there's a good chance that Norges Bank is much more worried about the economy than most of us realize. One sign of this is how they today expressed their concern for the world economy:

"The upturn in the world economy remains moderate and there is considerable uncertainty surrounding developments ahead."

As of late, one of the main arguments for an expected soft landing in Norway has been the strength of world economy, a factor which, combined with a weaker Krone, is expected to help Norwegian non-oil exporters. The oil price fall has been widely interpreted as being supply-related, which would mean it would stimulate oil-importing economies. That is a dangerous over-simplification. You can never forget the demand side, and there it is expectations that matter. China, one of the main locomotives of world economy since 2008, has been slowing down for a while and this trend is expected to continue in 2015. Europe is another headache that won't go away, and it's the destination for around 80 % of Norwegian exports.

It has been suggested that today's rate cut is a sign of strong pessimism on the part of Norges Bank, and I can't but agree. To be fair, Dørum of DNB says that if credit growth would slow down substantially, then a rate cut could be the right choice. Whereas he would like to see more evidence before the cut, Norges Bank has decided to act already on the expectation of much slower credit growth. In other words, it's trying to do "whatever it takes" (please, Mr. Olsen, don't ever use those words...) to stay ahead of the curve.

I see also a human factor behind this decision. This might come as a revelation for some of the readers, but central bankers are human beings like the rest of us. To better understand what they might be thinking at Norges Bank, I suggest you read this article from the Financial Times: "Central banks: Stockholm syndrome". It shows how Sweden's Riksbank, and especially its head Stefan Ingves, has been crucified -- by Paul Krugman and the likes -- for too tight monetary policy, the aim of which was to fight credit growth and higher home prices. I do recognize that the inflation and unemployment situation is different in Norway at the moment. But so is it with GDP growth (6,6 per cent in Sweden back in 2010!) and the expectations thereof. My point is a broader one: In the current environment, the prevailing (academic) opinion -- which I disagree with -- makes it very likely that central bankers will get punished for anything that in retrospect turns out to be too tight monetary policy. This has happened to Riksbank under Ingves in 2010 and the ECB under Trichet in 2011.

Whether we like it or not, the "easing bias", much critized by the Bank for International Settlements, is still there. But I can live with a 0,25 point cut, which I don't expect to be enough to keep the credit flowing freely to households now that the severity of the economic situation is finally dawning on the public. Should I find myself mistaken on this one later, I promise to curse today's rate cut!

UPDATE: Olsen puts it like this at Bloomberg:

“Our job now is that we need to prevent a severe downturn in the economy”

Tuesday, December 9, 2014

Norwegian Housing Market: What To Expect In 2015

The baseline scenario in my opinion is clear: I don't see any reason to rush to buy at this point. One can be fairly

sure that there won't be any runaway home price inflation, which means

that the upside is much more limited than the downside. If one expects

interest rates to move from 3,0 % towards 2,0 %, it will make little

difference if one at the same time expects home prices to drop 10-20 %.

One just doesn't buy in that situation. I think the market will become a

lot more price sensitive, a situation where we really haven't been save

autumn last year.

"It's only the sentiment" story -- which basically relied on Norwegians looking in the mirror and seeing themselves as irrational pessimists -- worked last winter, combined with banks pushing out loans again, but now the storyline needs to change. "It's only the fundamentals" isn't as convincing, is it? Not from a homebuyer perspective, and not from a bank shareholder -- and, even tougher, creditor -- perspective. Well, DNB might be a bit different, due to its market share and high government ownership. If Rune Bjerke, this Jamie Dimon of Norway, decides that the first-time buyers should be there to support the market, and Norges Bank and Finanstilsynet either play along or get pushed aside by democratic forces (the government with voters' backing), then who knows. (Of course I exaggerate, and I'm no "conspiracy theorist", but I think there could be more than a grain of truth in this when we look at what has happened this year...) It's very hard to do any guessing regarding when the banks will need to tighten their purses, but the risk of that happening this winter can't be negligible taken into account the current economic situation and, more importantly, the expectations.

The problem with economics is that you can always build a very convincing "doomsday scenario", because there are very real feedback loops in the economy. Just a short example:

Less lending will lead to lower home prices. Lower home prices will lead to even less lending, less construction, higher unemployment, lower salaries, less consumption, again higher unemployment, lower salaries, lower home prices, less lending... (See Irving Fisher's famous "Debt-Deflation Theory")

You continue this thought exercise for long enough and you end up with Norway turning into Venezuela... something that is very unlikely to happen, either because we find a natural "equilibrium" before we reach that point, or because there will be a successful government intervention (some economists are still arguing about which one it is). You probably get a more realistic picture when you look at the history and countries around you. To expect Norway to look a bit more like Denmark, or the Netherlands, in a couple of years might be more realistic. It's painful nevertheless, as people would feel a lot poorer than they do today.

Professor Hilde C. Bjørnland, I have understood, is someone who has worked to better understand how the weakness, and -- one should never forget -- the strength, in oil sector might feed to Norwegian economy in general. How I would sum it up here (for dummies like myself) is that we shouldn't think the rest of the economy is isolated, and the public sector especially has been affected (perhaps "bloated" could be the right word here) by the oil boom -- a fact that will make it vulnerable, or less agile, when the need comes to stimulate the economy while (especially oil-related) tax income is falling fast. I stress that these are my words, and you should check her work with Leif Anders Thorsrud to form your own opinion: "Ringvirkninger: Norsk økonomi og olje", November 2013. (I couldn't find any English version, sorry).

But what is true about the possibilities for building a "doomsday scenario" is also true about the opposite, what is often called a "Goldilocks scenario". So I think it would be very naive, bordering ridiculous, to expect that the fall in oil prices, oil jobs and oil income will be offset by the stimulative effect that lower oil prices might have in oil importing economies, combined with a weaker Krone, a combination which can lead to higher exports for Norwegian non-oil businesses. First, we don't even know to how large extent the oil price is now falling because demand is falling (look at China, especially -- my favorite "culprit" when it comes to volatility in commodity prices). It's not only the supply increases that are behind this price fall, so other economies might be weakening too. But most important of all, you just can't have the cake and eat it too: In my opinion one can by all means expect the negative effect of oil price drop to be offset, but only to the extent that one believes that the effect of higher oil prices on the Norwegian economy during the least 15 years has been offset by the drag of higher prices on the oil importing economies, and the stronger Krone.

Hope for the best, plan for the worst. It's all about probabilities, not about certainties.

Full disclosure: As you know, I was quite sure that home prices would fall already in 2014. It cost me a bottle of champagne. But Baard Schumann, the CEO of one of the largest homebuilders in Norway, was fair enough to renew the bet for 2015. This means that I have again a bottle of champagne to lose or gain depending on if home prices in December 2015 will be lower than 12 months before. I don't have other similar bets ongoing, nor will I take any.

"It's only the sentiment" story -- which basically relied on Norwegians looking in the mirror and seeing themselves as irrational pessimists -- worked last winter, combined with banks pushing out loans again, but now the storyline needs to change. "It's only the fundamentals" isn't as convincing, is it? Not from a homebuyer perspective, and not from a bank shareholder -- and, even tougher, creditor -- perspective. Well, DNB might be a bit different, due to its market share and high government ownership. If Rune Bjerke, this Jamie Dimon of Norway, decides that the first-time buyers should be there to support the market, and Norges Bank and Finanstilsynet either play along or get pushed aside by democratic forces (the government with voters' backing), then who knows. (Of course I exaggerate, and I'm no "conspiracy theorist", but I think there could be more than a grain of truth in this when we look at what has happened this year...) It's very hard to do any guessing regarding when the banks will need to tighten their purses, but the risk of that happening this winter can't be negligible taken into account the current economic situation and, more importantly, the expectations.

The problem with economics is that you can always build a very convincing "doomsday scenario", because there are very real feedback loops in the economy. Just a short example:

Less lending will lead to lower home prices. Lower home prices will lead to even less lending, less construction, higher unemployment, lower salaries, less consumption, again higher unemployment, lower salaries, lower home prices, less lending... (See Irving Fisher's famous "Debt-Deflation Theory")

You continue this thought exercise for long enough and you end up with Norway turning into Venezuela... something that is very unlikely to happen, either because we find a natural "equilibrium" before we reach that point, or because there will be a successful government intervention (some economists are still arguing about which one it is). You probably get a more realistic picture when you look at the history and countries around you. To expect Norway to look a bit more like Denmark, or the Netherlands, in a couple of years might be more realistic. It's painful nevertheless, as people would feel a lot poorer than they do today.

Professor Hilde C. Bjørnland, I have understood, is someone who has worked to better understand how the weakness, and -- one should never forget -- the strength, in oil sector might feed to Norwegian economy in general. How I would sum it up here (for dummies like myself) is that we shouldn't think the rest of the economy is isolated, and the public sector especially has been affected (perhaps "bloated" could be the right word here) by the oil boom -- a fact that will make it vulnerable, or less agile, when the need comes to stimulate the economy while (especially oil-related) tax income is falling fast. I stress that these are my words, and you should check her work with Leif Anders Thorsrud to form your own opinion: "Ringvirkninger: Norsk økonomi og olje", November 2013. (I couldn't find any English version, sorry).

But what is true about the possibilities for building a "doomsday scenario" is also true about the opposite, what is often called a "Goldilocks scenario". So I think it would be very naive, bordering ridiculous, to expect that the fall in oil prices, oil jobs and oil income will be offset by the stimulative effect that lower oil prices might have in oil importing economies, combined with a weaker Krone, a combination which can lead to higher exports for Norwegian non-oil businesses. First, we don't even know to how large extent the oil price is now falling because demand is falling (look at China, especially -- my favorite "culprit" when it comes to volatility in commodity prices). It's not only the supply increases that are behind this price fall, so other economies might be weakening too. But most important of all, you just can't have the cake and eat it too: In my opinion one can by all means expect the negative effect of oil price drop to be offset, but only to the extent that one believes that the effect of higher oil prices on the Norwegian economy during the least 15 years has been offset by the drag of higher prices on the oil importing economies, and the stronger Krone.

Hope for the best, plan for the worst. It's all about probabilities, not about certainties.

Full disclosure: As you know, I was quite sure that home prices would fall already in 2014. It cost me a bottle of champagne. But Baard Schumann, the CEO of one of the largest homebuilders in Norway, was fair enough to renew the bet for 2015. This means that I have again a bottle of champagne to lose or gain depending on if home prices in December 2015 will be lower than 12 months before. I don't have other similar bets ongoing, nor will I take any.

Tuesday, October 7, 2014

Just The Sentiment?

It seems my "summer holiday" gets longer and longer with every passing year... Perhaps my habits would fit better book-writing than blogging? Well, here we go.

Where are we today, and where did we come from? When I look at the past ~15 months in the Norwegian housing market, and the economy in general, what catches my eye is an interesting interplay between fundamentals and sentiment. It's actually hard not to see a fair dose of irony in it. Let me tell you what I mean.

Last autumn, when home prices were in decline and "It's a bubble!" folks were already practising their I-told-you-so's, Statistics Norway and some other market commentators were telling us how the price fall was driven by weak sentiment, or market psychology. According to them, people had taken an irrationally negative view on the housing market, but the effect of this would be short-lived as the fundamentals (e.g. GDP and income growth, employment) remained strong. Back then, I argued that this is not true, that the fundamentals are widely expected to weaken, with investment flattening out and growth slowing, and it's these expectations that should, and do, affect the market. Well, I haven't changed my mind since, but the panic in the housing market did end up being fairly short-lived, just like these commentators were suggesting.

Now, in autumn 2014, these "It's just the sentiment" commentators are increasingly facing a dilemma:

The fundamentals are weakening (just like many expected in 2013) and, as of late, strikingly so. Oil-related investments could be reduced by 10-15 % in 2015 if we are to believe the consensus (no talk of flattening out here...), and these expectations have mostly been formed before last week's sharp drop in oil price. The financial media in Norway is full of reports of oil (service) companies cutting workforce and analysts telling how the Oil Age is over, at least for now. And if this isn't gloomy enough, the EU (destination for ~80 % of Norwegian exports) is again teetering on the brink of a recession. Meanwhile, the sentiment on the housing market seems to be fairly strong, with year-on-year price growth around 3,6 %. The astounding certainty over positive home price development, a certainty which was hurt in late 2013, seems to be fully re-established.

So, how is it this time - should we expect the sentiment to catch up with the fundamentals? Is it now irrational to believe, like many still do, that one should buy an apartment even when it's only for the duration of a three-year study? Is it likewise irrational to think that home prices are prevented from falling by high population growth, when population growth (net migration) has been so closely correlated with the growth in oil investments (and jobs) in 2000-2014?

Where are we today, and where did we come from? When I look at the past ~15 months in the Norwegian housing market, and the economy in general, what catches my eye is an interesting interplay between fundamentals and sentiment. It's actually hard not to see a fair dose of irony in it. Let me tell you what I mean.

Last autumn, when home prices were in decline and "It's a bubble!" folks were already practising their I-told-you-so's, Statistics Norway and some other market commentators were telling us how the price fall was driven by weak sentiment, or market psychology. According to them, people had taken an irrationally negative view on the housing market, but the effect of this would be short-lived as the fundamentals (e.g. GDP and income growth, employment) remained strong. Back then, I argued that this is not true, that the fundamentals are widely expected to weaken, with investment flattening out and growth slowing, and it's these expectations that should, and do, affect the market. Well, I haven't changed my mind since, but the panic in the housing market did end up being fairly short-lived, just like these commentators were suggesting.

Now, in autumn 2014, these "It's just the sentiment" commentators are increasingly facing a dilemma:

The fundamentals are weakening (just like many expected in 2013) and, as of late, strikingly so. Oil-related investments could be reduced by 10-15 % in 2015 if we are to believe the consensus (no talk of flattening out here...), and these expectations have mostly been formed before last week's sharp drop in oil price. The financial media in Norway is full of reports of oil (service) companies cutting workforce and analysts telling how the Oil Age is over, at least for now. And if this isn't gloomy enough, the EU (destination for ~80 % of Norwegian exports) is again teetering on the brink of a recession. Meanwhile, the sentiment on the housing market seems to be fairly strong, with year-on-year price growth around 3,6 %. The astounding certainty over positive home price development, a certainty which was hurt in late 2013, seems to be fully re-established.

So, how is it this time - should we expect the sentiment to catch up with the fundamentals? Is it now irrational to believe, like many still do, that one should buy an apartment even when it's only for the duration of a three-year study? Is it likewise irrational to think that home prices are prevented from falling by high population growth, when population growth (net migration) has been so closely correlated with the growth in oil investments (and jobs) in 2000-2014?

Sunday, May 4, 2014

A Cliffhanger Moment?

As you have noticed, I've been deeply engaged lately in another project related to my main interest, which is money and debt. I'll start blogging about it very soon, and I hope that I get some feedback from especially the readers who share my interest - I've spotted many of you already in the comments section of this blog. I'll post a link when I'm online.

I don't go into details regarding the housing market in February-April, but the market hasn't been as weak as some had anticipated. To be honest, I myself anticipated a weaker market as well, but then again, I usually do that because things seem so obvious to me that I assume other people must see it somewhat the same way ;-) But in no way is the market exceptionally strong. The prices, as is typical in spring, are rising (12-month growth is back to positive at 0,3 % in March). Pricewise the market has been fairly strong, but supply side is where I see the ultimate weakness which I also referred to in my previous post. There were many signs earlier in the year that some willing sellers are holding back and waiting for demand to get higher, or supply lower (often two sides of the same coin), and I think this will keep the supply high going forward. I struggle to see where the demand that could eat up this inventory could come, but we are surely wiser after May and June.

There are also signs that banks are more willing to lend and have reduced mortgage rates slightly. My explanation for this development at the moment is that this is what the banks have to do if they want to deliver profits in the short-term. Many Norwegian banks depend so heavily, directly or indirectly, on the forever rising housing market, that they are in a sense "all in". They surely feel it's like shooting their own foot if they would start to really limit lending now. In the end, it's Norges Bank who needs to take the tough decisions. What I assume NB is thinking now - at least I would be - is that it's probably best to see how the housing (and lending) market will develop going forward in 2014. If the seeds for a price fall have already been sown, then it's best to do no drastic moves at this moment. What they probably want to see is stagnating prices, for now. What they are more worried about, though, is growth in lending. This has been falling since autumn, although it's still well above 6 %. I expect Finanstilsynet (bank supervisor) to keep up the strict rhetoric and make sure that banks are not relaxing their lending standards.

Overall, I would dare to say that the authorities are trying to set a ceiling for the home prices, or at least limit the growth to very low single digits. The only way for the price growth to get out of control again is a deficit in housing units available, and I've made it clear already that I can't see where this would come from. There is a flood of new homes coming on the market throughout 2014 and the supply of existing dwellings is also high. Job-based immigration is falling, so it's hard to see the demand for housing growing, especially now that people have become more careful with buying. At the moment, I expect that 2014 will play out in a fairly similar way 2013 did, with prices starting to fall again soon. I must admit that I didn't expect this a couple of months ago - I expected worse. And it still can turn worse (or better), depending on how the world economy (not least China) will develop.

If I let my imagination free, I could say that we might also be witnessing here a partly self-fulfilling prognosis from various players in the market, not least Statistics Norway and Norges Bank. They forecasted a dip, and now that the banks seem to be playing along, the broader expectation might be that this will work out like forecasted. This won't have a lasting effect, though, if what is wrong with the market is not just market psychology, but, like I have argued, there are fundemental reasons (a slowing economy) behind the price fall in 2013.

Thursday, February 20, 2014

Population Growth Falling

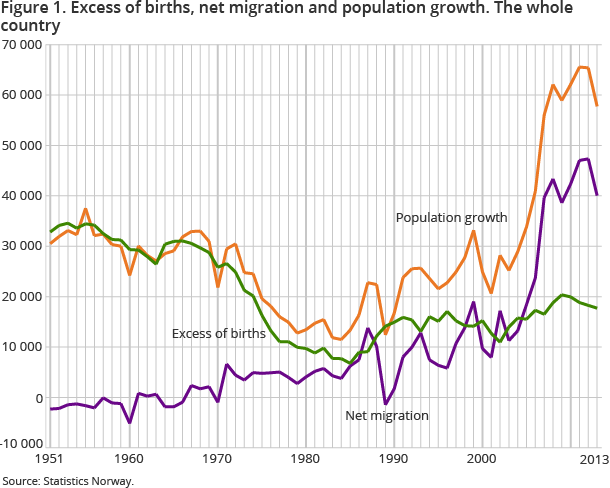

In April 2013 I wrote about the net migration and it's effect on Norwegian home prices. I have mentioned earlier that there is a strong belief in Norway that not enough new homes are built to meet the demand for housing. This argument is used so often in media that it has more or less become "conventional wisdom". The underlying forecasts of high future demand are mainly based on assumption of continuing high net migration.

Steinar Juel from Nordea Bank is among the few who have questioned this conventional wisdom. In a report from Oct'13 (in Norwegian), he takes up the rising amount of homes for sale as one indicator of a supply that meets the demand, and also points, like I did, to the volatile net migration.

Per Jæger of the homebuilders' assocation Boligprodusentene is pointing to yearly population growth of around 60 000 to 70 000, of which around 70 % has been due to net migration, and says that we should be building around 38 000 homes per year (and again adds that "it's illogical to think that home prices will fall"). Here he naturally needs to make an assumption on the household size. While the average size of a household in Norway is 2,2 persons, it is clear that migrants with lower income live in bigger households. Chris McDonald of Reserve Bank of New Zealand has found in his study that one additional house is build for around every six migrants in New Zealand. The actual number doesn't need to be even close to this high to make the assumptions of homebuilders questionable.

But that's not all. Today we got a report on population trends in 2013 from Statistics Norway and here's the updated "hockey stick":

SSB writes:

The implications of lower population growth on housing demand can be significant. There is an impact both directly and indirectly (through lower demand for rental units) on the amount of home buyers in the market. Polish and Lithuanian citizens are the two largest groups of immigrants. Many of these occupy jobs related to construction and home repairs/maintenance. As the housing starts started to fall only in the end of 2013 (down 17,5 % year-on-year in Q4'13 and a whopping 37 % in Jan'14!), we don't yet see the real effect of a most likely negative job growth in the construction sector in the migration statistics. If the new home sales and housing starts don't improve soon, there will be little doubt about which direction the population growth will go in 2014.

It might be that 2014 will be remembered as the year when the big story of housing deficit (boligmangel) was finally buried?

Steinar Juel from Nordea Bank is among the few who have questioned this conventional wisdom. In a report from Oct'13 (in Norwegian), he takes up the rising amount of homes for sale as one indicator of a supply that meets the demand, and also points, like I did, to the volatile net migration.

Per Jæger of the homebuilders' assocation Boligprodusentene is pointing to yearly population growth of around 60 000 to 70 000, of which around 70 % has been due to net migration, and says that we should be building around 38 000 homes per year (and again adds that "it's illogical to think that home prices will fall"). Here he naturally needs to make an assumption on the household size. While the average size of a household in Norway is 2,2 persons, it is clear that migrants with lower income live in bigger households. Chris McDonald of Reserve Bank of New Zealand has found in his study that one additional house is build for around every six migrants in New Zealand. The actual number doesn't need to be even close to this high to make the assumptions of homebuilders questionable.

But that's not all. Today we got a report on population trends in 2013 from Statistics Norway and here's the updated "hockey stick":

SSB writes:

The population growth was 1.1 per cent in 2013, which is the smallest percentage growth in Norway since 2006. Net migration from abroad decreased by 7 200 from 2012 to 2013 - down from 47 300 to 40 100, and this is the lowest since 2009.

The implications of lower population growth on housing demand can be significant. There is an impact both directly and indirectly (through lower demand for rental units) on the amount of home buyers in the market. Polish and Lithuanian citizens are the two largest groups of immigrants. Many of these occupy jobs related to construction and home repairs/maintenance. As the housing starts started to fall only in the end of 2013 (down 17,5 % year-on-year in Q4'13 and a whopping 37 % in Jan'14!), we don't yet see the real effect of a most likely negative job growth in the construction sector in the migration statistics. If the new home sales and housing starts don't improve soon, there will be little doubt about which direction the population growth will go in 2014.

It might be that 2014 will be remembered as the year when the big story of housing deficit (boligmangel) was finally buried?

Thursday, February 13, 2014

The Norwegian Bubble in Facebook and Twitter

There has been some traffic coming in from Facebook, so I thought it's best to create a presence there finally. Please "like" and spread the word if you agree with the content! I'll try to come up with real content soon again ;-)

Facebook: http://www.facebook.com/norwegianbubble

Twitter: http://twitter.com/catonyourface

Facebook: http://www.facebook.com/norwegianbubble

Twitter: http://twitter.com/catonyourface

Wednesday, February 5, 2014

Change In The Way EFF House Price Index Is Calculated

Here's a comparison between the new index (published Jan'14) and the old index (published Dec'13, indexed by me, Jan'03=1,00) from January 2012 to December 2013 (the last month we have old index data for):

Notice how the monthly fluctuations follow a new pattern. The gap between the new index and the old index (new minus old) is not stable as you can see from this graph (data from Jan'10 to Dec'13):

Note especially the sharp change in January 2013. It looks like the high growth between January 2012 and January 2013 is smoothed down in the new index. The adjustment becomes again smaller throughout 2013, coinciding with sharply slowing growth.

I don't know yet what to think of this. What we can be sure of is that the Jan'13 adjustment gives us higher year-on-year growth in Jan'14 compared to what it would have been in the old index, or in the new index had the gap between the new and old been more stable. It also makes it more likely that year-on-year growth in Feb'14-May'14 will be significantly lower than it was in Jan'14 (-1,0 %, which was surprisingly strong...), doesn't it? Help me out here, quants :-)

And if you think I have done a "Reinhart-Rogoff" with my Excel, let me know as soon as possible.

Notice how the monthly fluctuations follow a new pattern. The gap between the new index and the old index (new minus old) is not stable as you can see from this graph (data from Jan'10 to Dec'13):

Note especially the sharp change in January 2013. It looks like the high growth between January 2012 and January 2013 is smoothed down in the new index. The adjustment becomes again smaller throughout 2013, coinciding with sharply slowing growth.

I don't know yet what to think of this. What we can be sure of is that the Jan'13 adjustment gives us higher year-on-year growth in Jan'14 compared to what it would have been in the old index, or in the new index had the gap between the new and old been more stable. It also makes it more likely that year-on-year growth in Feb'14-May'14 will be significantly lower than it was in Jan'14 (-1,0 %, which was surprisingly strong...), doesn't it? Help me out here, quants :-)

And if you think I have done a "Reinhart-Rogoff" with my Excel, let me know as soon as possible.

Sunday, February 2, 2014

High Loan-To-Value Mortgages And The Real Concern For The Norwegian Youth

During the last week or two I have participated in a debate over the Norwegian financial authorities' limit on high loan-to-value mortgages dating back to 2012. The limit is not absolute, but it pushes banks in most cases to require that the buyer of the property finances 15 % of the purchase with equity. In other words, it limits the mortgage to 85 % of property value. This is known as "egenkapitalkrav på 15 %" in Norwegian.

(For further information on reasons behind this kind of limit, I suggest you read this Bloomberg article by Peter Orszag. He looks at the newly imposed limit in New Zealand, but mentions also that Canada, Israel, Singapore and Sweden among others have similar limits.)

The public opinion in Norway until late has been strongly against the raised limit. Catering to this opinion helped the newly elected government to win the elections; the parties campaigned on reducing the limit back to 90 %/10 % were it stood earlier (although it was less strictly enforced back then, and 100 % loan-to-value mortgages weren't unheard of). For sure, this is a controversial tool, but then again, there are no perfect tools. In the end, the limit is criticized exactly because it achieves the goals it was meant to achieve. You need to evaluate the pros and cons of it to form an opinion on it. I'll start by presenting the cons taken up by the dominating side, before I move to the pros, and most importantly, the underlying reasons behind raising the limit.

Norway has a relatively egalitarian society, reflecting the strength of the Nordic social-democratic movement. People are for equal opportunity. Equal opportunity can be defined in many ways, and in Norway it clearly includes the opportunity to buy a home given that you have an income that can serve the loan. What creates inequality (klasseskille) is leaving people with less (inherited) resources on the rental market, where they pay for their housing a lot more than the homeowners do (not least thanks to the heavy tax benefits enjoyed by mortgage-holders). Add the enormous house price appreciation witnessed in Norway, and you get a feeling that the rich get richer and the poor get poorer, and it's hard to deny that it hasn't been the case during the last 20 years.

The main* argument against the 85 % limit is thus that it creates inequality by leaving the ones without large savings and/or financial help from parents on the rental market. And people here genuinely -- and somewhat understandably, when we take into account the recent history -- believe that one is always better off owning. The conclusion from this is that young people should be helped to "enter the market" as early as possible, so that they don't "waste" their money by renting.

The intentions behind the policy of high homeownership, especially among the less well-off, are no doubt good. But good intentions don't always lead to good outcomes. This policy was taken to one kind of extreme in the U.S. in early 2000, where it was one of the reasons behind the subprime crisis that started in 2007. The pursuit of high homeownership has been taken to an extreme in Norway too, although we shouldn't draw too many parallels between these two countries. Whereas in the U.S. it was the means that became extreme (subprime/NINJA loans), in Norway it has been the level of achievement that is in my opinion extreme.

Homeownership in Norway has achieved what one could almost describe as cult-/religion -like status, and the homeownership ratio stands at over 80 %. In the age group 30-34 year-olds, 74 % own their own home, in the group 25-29 year-olds 52 %, and even in the group 20-24 year-olds whole 19 % are homeowners (source: NIBR). These are mind-blowing numbers, many times higher than in most of the other developed countries. And compared to inhabitants of the other rich nations, Norwegians privately own relatively little financial assets like stocks and bonds. Most of their wealth is tied to the property market. For an outsider this might sound like a sign of a bubble, but for Norwegians the central role of the housing market is rather something to be proud of (this might explain why prime minister Solberg used the concentration of wealth on the housing market as an argument against a bubble, like I told earlier).

As I have stated on earlier occasions, I'm concerned for the Norwegian youth. It's clear that there is a risk related to taking a mortgage with a high loan-to-value ratio. The house prices do fall, and sometimes significantly.

According to the latest review of banks' lending practises from fall 2013 (see Finanstilsynet, in Norwegian), the loan-to-value ratio exceeds 85 % in 35 % of mortgages to under 35 year-olds. In 12 % of the youth's mortgages the loan-to-value ratio exceeds 100 %.

These are young people who have the most productive decades of their life right in front of them. According to NIBR, 52 % of 20-34 year-olds are homeowners. Of these, according to Finanstilsynet, 35 % have mortgages where the loan-to-value ratio exceeds 85 %. This is where in my opinion the biggest risk to Norwegian economy lies. Many of these young people have seen no alternative to owning. And the state and the banks have taken care that an internationally disproportionate share of them get to own -- by providing them with easy credit.

I'm not the only one who is worried that the young people who have been helped to the market might end up getting hurt. The 85 % limit is there because Norwegian and international financial authorities, among others, directly or indirectly (through bubble concern) share my concern for the Norwegian youth. This includes Norges Bank, Finanstilsynet, Ministry of Finance, IMF, OECD, and so far three Nobel laureates in economics. (Some evidence here, here** and for example here.) Do these authorities, or I, know for sure that the house prices will fall significantly? No. But we know that the risk of this happening is real. We know that no one should state that they help the young people by providing them with easy credit, so that they can buy property that according to many indicators is already overvalued.

So here are the two sides to this debate (somewhat tongue-in-cheek, if you allow):

Team A: "We're helping the young people by calling for easier access to credit"

Members:

Mostly homebuilders and real-estate agents (!) since the house prices started to fall.

Team B: "We're helping the young people and the Norwegian economy by restricting access to credit"

Members:

Norges Bank

Finanstilsynet

IMF

OECD

Yours truly

It's time for you to choose your side.

---------------------------------------------------------

* Some people more understandably oppose the limit on the grounds of negative consequences of government intervention in the markets. It's another story, but I think you don't want to start here if you want to free the markets from government intervention. A free market is not reality, and banks don't need to behave like they would behave in a free market. Instead, they have very strong (perhaps short-term, but nevertheless) incentives to lend out more freely than is healthy for the economy.

** This is a very important article in that it reveals what the government really thinks about the housing market. I think we can thank the new finance minister Jensen for saying out loud something that she and the prime minister Solberg since have tried to downplay in public; there is a real concern for the housing market. This perhaps also explains why the government didn't even try to keep it's promise to take the limit back to 90 %/10 %.

(For further information on reasons behind this kind of limit, I suggest you read this Bloomberg article by Peter Orszag. He looks at the newly imposed limit in New Zealand, but mentions also that Canada, Israel, Singapore and Sweden among others have similar limits.)

The public opinion in Norway until late has been strongly against the raised limit. Catering to this opinion helped the newly elected government to win the elections; the parties campaigned on reducing the limit back to 90 %/10 % were it stood earlier (although it was less strictly enforced back then, and 100 % loan-to-value mortgages weren't unheard of). For sure, this is a controversial tool, but then again, there are no perfect tools. In the end, the limit is criticized exactly because it achieves the goals it was meant to achieve. You need to evaluate the pros and cons of it to form an opinion on it. I'll start by presenting the cons taken up by the dominating side, before I move to the pros, and most importantly, the underlying reasons behind raising the limit.

Norway has a relatively egalitarian society, reflecting the strength of the Nordic social-democratic movement. People are for equal opportunity. Equal opportunity can be defined in many ways, and in Norway it clearly includes the opportunity to buy a home given that you have an income that can serve the loan. What creates inequality (klasseskille) is leaving people with less (inherited) resources on the rental market, where they pay for their housing a lot more than the homeowners do (not least thanks to the heavy tax benefits enjoyed by mortgage-holders). Add the enormous house price appreciation witnessed in Norway, and you get a feeling that the rich get richer and the poor get poorer, and it's hard to deny that it hasn't been the case during the last 20 years.

The main* argument against the 85 % limit is thus that it creates inequality by leaving the ones without large savings and/or financial help from parents on the rental market. And people here genuinely -- and somewhat understandably, when we take into account the recent history -- believe that one is always better off owning. The conclusion from this is that young people should be helped to "enter the market" as early as possible, so that they don't "waste" their money by renting.

The intentions behind the policy of high homeownership, especially among the less well-off, are no doubt good. But good intentions don't always lead to good outcomes. This policy was taken to one kind of extreme in the U.S. in early 2000, where it was one of the reasons behind the subprime crisis that started in 2007. The pursuit of high homeownership has been taken to an extreme in Norway too, although we shouldn't draw too many parallels between these two countries. Whereas in the U.S. it was the means that became extreme (subprime/NINJA loans), in Norway it has been the level of achievement that is in my opinion extreme.

Homeownership in Norway has achieved what one could almost describe as cult-/religion -like status, and the homeownership ratio stands at over 80 %. In the age group 30-34 year-olds, 74 % own their own home, in the group 25-29 year-olds 52 %, and even in the group 20-24 year-olds whole 19 % are homeowners (source: NIBR). These are mind-blowing numbers, many times higher than in most of the other developed countries. And compared to inhabitants of the other rich nations, Norwegians privately own relatively little financial assets like stocks and bonds. Most of their wealth is tied to the property market. For an outsider this might sound like a sign of a bubble, but for Norwegians the central role of the housing market is rather something to be proud of (this might explain why prime minister Solberg used the concentration of wealth on the housing market as an argument against a bubble, like I told earlier).

The real concern for the Norwegian youth

As I have stated on earlier occasions, I'm concerned for the Norwegian youth. It's clear that there is a risk related to taking a mortgage with a high loan-to-value ratio. The house prices do fall, and sometimes significantly.

According to the latest review of banks' lending practises from fall 2013 (see Finanstilsynet, in Norwegian), the loan-to-value ratio exceeds 85 % in 35 % of mortgages to under 35 year-olds. In 12 % of the youth's mortgages the loan-to-value ratio exceeds 100 %.

These are young people who have the most productive decades of their life right in front of them. According to NIBR, 52 % of 20-34 year-olds are homeowners. Of these, according to Finanstilsynet, 35 % have mortgages where the loan-to-value ratio exceeds 85 %. This is where in my opinion the biggest risk to Norwegian economy lies. Many of these young people have seen no alternative to owning. And the state and the banks have taken care that an internationally disproportionate share of them get to own -- by providing them with easy credit.

I'm not the only one who is worried that the young people who have been helped to the market might end up getting hurt. The 85 % limit is there because Norwegian and international financial authorities, among others, directly or indirectly (through bubble concern) share my concern for the Norwegian youth. This includes Norges Bank, Finanstilsynet, Ministry of Finance, IMF, OECD, and so far three Nobel laureates in economics. (Some evidence here, here** and for example here.) Do these authorities, or I, know for sure that the house prices will fall significantly? No. But we know that the risk of this happening is real. We know that no one should state that they help the young people by providing them with easy credit, so that they can buy property that according to many indicators is already overvalued.

So here are the two sides to this debate (somewhat tongue-in-cheek, if you allow):

Team A: "We're helping the young people by calling for easier access to credit"

Members:

Mostly homebuilders and real-estate agents (!) since the house prices started to fall.

Team B: "We're helping the young people and the Norwegian economy by restricting access to credit"

Members:

Norges Bank

Finanstilsynet

IMF

OECD

Yours truly

It's time for you to choose your side.

---------------------------------------------------------

* Some people more understandably oppose the limit on the grounds of negative consequences of government intervention in the markets. It's another story, but I think you don't want to start here if you want to free the markets from government intervention. A free market is not reality, and banks don't need to behave like they would behave in a free market. Instead, they have very strong (perhaps short-term, but nevertheless) incentives to lend out more freely than is healthy for the economy.

** This is a very important article in that it reveals what the government really thinks about the housing market. I think we can thank the new finance minister Jensen for saying out loud something that she and the prime minister Solberg since have tried to downplay in public; there is a real concern for the housing market. This perhaps also explains why the government didn't even try to keep it's promise to take the limit back to 90 %/10 %.

Thursday, January 9, 2014

Paul Krugman vs. Erna Solberg

Paul Krugman has managed to stir some public debate again. He came to Norway and stated what almost any economist would state at this point -- pretty much what Robert Shiller had said already in 2012 and Vernon Smith in 2013 --, namely that this looks like a housing bubble. That makes it now three Nobelists. Krugman, who is not exactly a person who tries to avoid confrontation at all costs, must have been nevertheless surprised by what followed:

No other than the prime minister, Erna Solberg, replied to Krugman and denied the existence of a bubble. Norway is different and foreign economists don't understand it. The usual stuff.

And this time Krugman wasn't even provocative in his comments! It seems in Norway mere mentioning the word "bubble" is provocative enough? This reminds me of what Jeremy Grantham of GMO, a renowned investor, said in a Wall Street Journal interview:

I'd say Norway compares with Australia in this matter. Overall, there's of course nothing bad in being optimistic. One could argue even the opposite. It's just that it's not really helpful if your goal is to avoid a bubble, is it?

Not surprisingly, it didn't take long until the "propaganda machine" of real estate brokers and homebuilders was lined behind the prime minister. I've got to say it amuses me how these guys, many of whose business has started to cool down and who believe in the "it's the negative sentiment, stupid" story (and continue to be proponents of the "we're not building enough" story), start tearing their hair out when faced with bubble suggestions and come out with their often weak arguments. Another clear sign of a bubble?

Guys, you can't argue against a bubble by just presenting the factors that prove that Norway is different. To argue against a bubble you need to show us how much higher price level those factors can support and that that price level is not yet exceeded. It's the price where the bubble always is. Your arguments could (and probably would) be used as well to justify a price 50 % above the current level.

The foreign economists look at indicators like price-to-rent, price-to-income and debt-to-income exactly because they don't want to get entangled in country-specific factors. You are denying the warning messages derived from these common indicators by relying on nothing else than country-specific factors. That often leads to a conclusion that "this time is different", and that's what these economists have learned to be afraid of.

So if you tell me Norway is rich, I say it's probably reflected in the price level already. Incomes are high? Debt-to-income is already around 210 %, close to world record levels. You say you're not starting to build new houses before 70 % of them are sold in advance? I say that this practice keeps the supply fairly tight, and a tight supply leads to higher prices. You think you can avoid a substantial fall in prices by keeping the supply tight? It's hard when you've contributed to the bubble with the very same practice. In addition, it's very hard to forecast the future need for housing, as work-based immigration to Norway is of cyclical nature. And forget the "people are moving into cities" argument. It's been the same in every country that has experienced a housing crash during the last 10 if not 30 years. This argument might very well have contributed to the bubble, like the bigger-than-national price decline now experienced in Oslo suggests.

In the article Erna Solberg is quoted arguing against a bubble by saying that in Norway there is one asset people put their savings in and take loans against, and it's housing. Isn't this a weakness, not a strength?

Denying a bubble outright is not smart. Being afraid of a bubble is smart. Former contributes to a bubble, the latter helps in avoiding it. So which one do you choose? Denying a bubble is of course a natural reaction from someone who is shit-scared of a bubble and thinks that negative sentiment can lead to a crash.

Let's face it. The government is obviously "very concerned with the housing market", as the outspoken new finance minister, Siv Jensen, told in October (neither denying nor confirming a bubble). This is fully in line with the concern for a bubble the previous prime minister, Jens Stoltenberg, aired already more than two years ago. So either Erna Solberg's comments were based on her private opinions, or then she is trying to calm people down. If the latter is true, we all should be worried. This is what Krugman probably referred to when he said that it's a sign of a bubble that politicians come out and say everything is OK.

I have a message to these people who use their expert -- or authoritative -- position to directly or indirectly push people to buy their first home or invest their savings in a rental apartment: If this turns out to be a bubble and there's a 20-40 % decline in the coming years, you should be ashamed. What you are telling people who are facing a big and very risky financial decision is that there's not really any risk there.

No other than the prime minister, Erna Solberg, replied to Krugman and denied the existence of a bubble. Norway is different and foreign economists don't understand it. The usual stuff.

And this time Krugman wasn't even provocative in his comments! It seems in Norway mere mentioning the word "bubble" is provocative enough? This reminds me of what Jeremy Grantham of GMO, a renowned investor, said in a Wall Street Journal interview:

"America is a very, very optimistic-biased society, as I believe, incidentally, Australia is, for whatever that means. We're the two great optimistic societies. You can have a conversation about a housing bubble in England, and they'll say, 'oh, is that right? Let me see the data.' If you have one in Australia, you have World War III! They hate you. They hate you for years! [laughs] The idea that you could suggest that they were having a housing bubble. [laughs]"

I'd say Norway compares with Australia in this matter. Overall, there's of course nothing bad in being optimistic. One could argue even the opposite. It's just that it's not really helpful if your goal is to avoid a bubble, is it?

Not surprisingly, it didn't take long until the "propaganda machine" of real estate brokers and homebuilders was lined behind the prime minister. I've got to say it amuses me how these guys, many of whose business has started to cool down and who believe in the "it's the negative sentiment, stupid" story (and continue to be proponents of the "we're not building enough" story), start tearing their hair out when faced with bubble suggestions and come out with their often weak arguments. Another clear sign of a bubble?

Guys, you can't argue against a bubble by just presenting the factors that prove that Norway is different. To argue against a bubble you need to show us how much higher price level those factors can support and that that price level is not yet exceeded. It's the price where the bubble always is. Your arguments could (and probably would) be used as well to justify a price 50 % above the current level.

The foreign economists look at indicators like price-to-rent, price-to-income and debt-to-income exactly because they don't want to get entangled in country-specific factors. You are denying the warning messages derived from these common indicators by relying on nothing else than country-specific factors. That often leads to a conclusion that "this time is different", and that's what these economists have learned to be afraid of.

So if you tell me Norway is rich, I say it's probably reflected in the price level already. Incomes are high? Debt-to-income is already around 210 %, close to world record levels. You say you're not starting to build new houses before 70 % of them are sold in advance? I say that this practice keeps the supply fairly tight, and a tight supply leads to higher prices. You think you can avoid a substantial fall in prices by keeping the supply tight? It's hard when you've contributed to the bubble with the very same practice. In addition, it's very hard to forecast the future need for housing, as work-based immigration to Norway is of cyclical nature. And forget the "people are moving into cities" argument. It's been the same in every country that has experienced a housing crash during the last 10 if not 30 years. This argument might very well have contributed to the bubble, like the bigger-than-national price decline now experienced in Oslo suggests.

In the article Erna Solberg is quoted arguing against a bubble by saying that in Norway there is one asset people put their savings in and take loans against, and it's housing. Isn't this a weakness, not a strength?

Denying a bubble outright is not smart. Being afraid of a bubble is smart. Former contributes to a bubble, the latter helps in avoiding it. So which one do you choose? Denying a bubble is of course a natural reaction from someone who is shit-scared of a bubble and thinks that negative sentiment can lead to a crash.

Let's face it. The government is obviously "very concerned with the housing market", as the outspoken new finance minister, Siv Jensen, told in October (neither denying nor confirming a bubble). This is fully in line with the concern for a bubble the previous prime minister, Jens Stoltenberg, aired already more than two years ago. So either Erna Solberg's comments were based on her private opinions, or then she is trying to calm people down. If the latter is true, we all should be worried. This is what Krugman probably referred to when he said that it's a sign of a bubble that politicians come out and say everything is OK.

I have a message to these people who use their expert -- or authoritative -- position to directly or indirectly push people to buy their first home or invest their savings in a rental apartment: If this turns out to be a bubble and there's a 20-40 % decline in the coming years, you should be ashamed. What you are telling people who are facing a big and very risky financial decision is that there's not really any risk there.

Subscribe to:

Posts (Atom)